Before all else, a note from our Founder & CEO

In our first quarter update of the year, we focus on the sector and how it has been able to hold steady as the winds of change have blown through by the Trump administration. Vuyani Bekwa, our Private Equity Principal, gives his views on the property sector and the major forces holding it up following the 29% benchmark increase in listed property for 2024. Enjoy.

THE SOUTH AFRICAN LISTED PROPERTY SECTOR: A NEW YEAR, NEW DYNAMICS – SA LISTED PROPERTY IN Q1 2025

The first quarter of 2025 is memorable for both global and South African markets. The US President Donald Trump started his second term in mid-January and immediately focused heavily on immigration and economic policies, including imposing tariffs on trading partners, which led to concerns about a potential global recession.

In South Africa, the FTSE/JSE All Share index, which tracks the performance of companies listed on the Johannesburg Stock Exchange, followed global markets, trending up 2.4%, Listed property suffered a loss of -3.0%, and was the only sector that delivered negative returns over the quarter this year, mostly due to some profit-taking after 2024’s stellar returns. The SA Reserve Bank loosened monetary policy after an extended period of restrictive policies reflected by high interest rates, while issues like geopolitical tensions and inflation continued to influence the landscape positively. The SA Reserve Bank cut interest rates by a further 25 basis points at the end of January, to align with international markets.

Here, we’ll dive into a straightforward overview of how things went in Q1 2025, including key economic trends, sector performance, and what to expect moving forward.

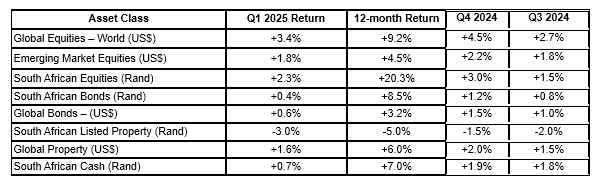

Asset Class Performance: Q1 2025 (1January – 31 March 2025)

GLOBAL MACRO CONTEXT AND MARKET TRENDS

The global economy has seen some big changes, with major central banks across the globe stepping in to try and boost economic growth. In the U.S., the Federal Reserve (Fed) cut interest rates by 1.0% (0.5% in September and another 0.5% in December). This drove the shift away from the restrictive policies which were prevailing and started to encourage more economic activity and support for the labour market while working on bringing inflation down to its 2% target. When Donald Trump was inaugurated in mid-January, markets started to run in anticipation of new policies which were expected to be more market friendly.

The US economy contracted by 0.3% in Q1 2025, marking the first decline since early 2022, attributed to escalating trade tensions and a surge in imports. The S & P 500 Index fell by 4.3% during the quarter, with nearly all the loss occurring in March, amid increased market volatility and uncertainty around tariffs. Global markets improved by 3.4% in Q1 2025. but saw divergent performance with Asian and Chinese markets showing resilience amid policy support, while the US faced economic contraction, and market declines due to trade tensions.

China set a real GDP growth target of around 5% for 2025 and adopted expansionary fiscal and monetary policies to boost domestic consumption. The MSCI China Index returned 15.02% in Q1 2025, reflecting strong performance in China’s capital markets, despite the tariff volatility.

Commodities reflected these shifts too: Brent crude oil prices dropped from $79.27/bbl to $71.74 /bbl (-9.4% in Q1 2025), driven by fears of reduced oil consumptions on the back of weakening global economic indicators and the impending trade war. Gold made a huge comeback (19.1%), increasing from $2,623 up to $3,123/oz, largely due to increasing global risk driven by the US stance on trading tariffs, and increasing uncertainties in the global economy. Property markets around the world showed mixed results: while lower rates boosted real estate in the U.S. and Europe, Japan and China still faced challenges, showing that recovery varies widely across regions.

SOUTH AFRICA’S MARKET SHIFTS

South Africa’s economy continued to be influenced by both local and international factors. The FTSE/JSE All Share Index, which reflects the performance of the companies on the Johannesburg Stock Exchange, climbed 2.4% in the first quarter, contributing to a 12-month gain of 20.3%. This growth was delivered due to perceived increased political stability with the formation of the Government of National Unity (GNU), a rise in investor confidence and a positive economic environment driven by a looser monetary stance due to lower inflation, with interest rates dropping by 75 basis points from its high in September 2024.

DIRECT PROPERTY SECTOR – PERFORMANCE AND INSIGHTS

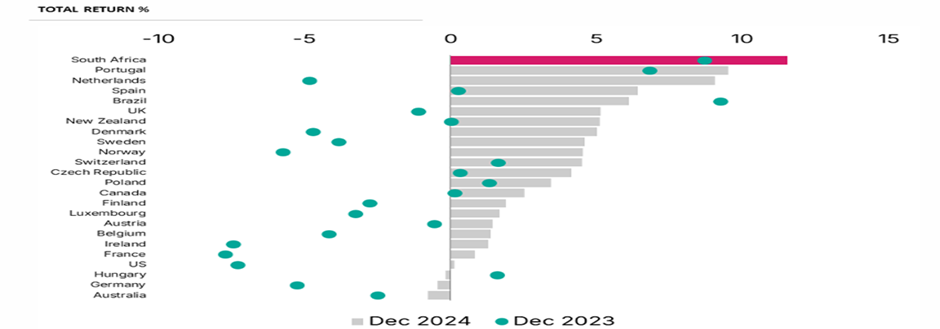

South African direct property returns were the highest globally over 2024 as highlighted by the graph below. This is nothing new as the returns were also strong in 2023, second only to Brazil.

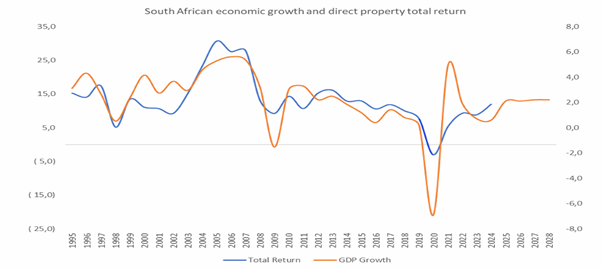

There is a strong correlation between GDP growth and total returns, ungeared direct property, and in our opinion, because GDP is expected to start picking up due to reduced loadshedding, a better economic environment (even though there are challenges) and lower interest rates, we think that the sector could deliver better returns going forward, which could translate to the listed property sector.

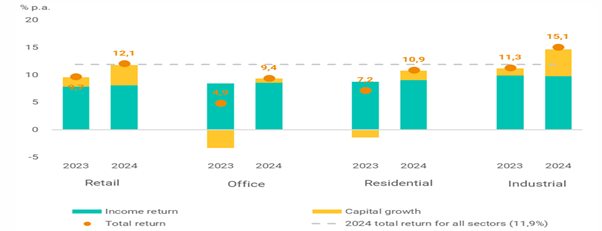

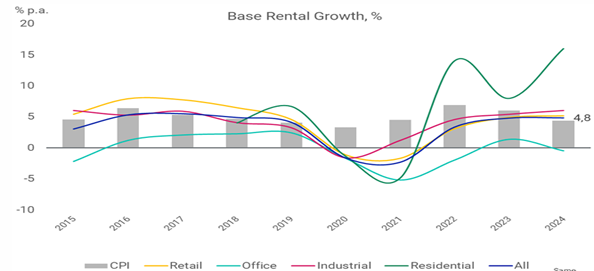

The total returns improved for each sector – with the industrial sector again showing the best total returns. As the economy is driven by financial services, manufacturing, exports, etc. and not just retail, the industrial sector should continue to perform well, especially since the consumer is struggling due to high interest rates, and a tough economy, hampered by high unemployment rates, and high administered prices.

RETAIL SECTOR: IMPROVING SENTIMENT AND ECONOMIC ENVIRONMENT

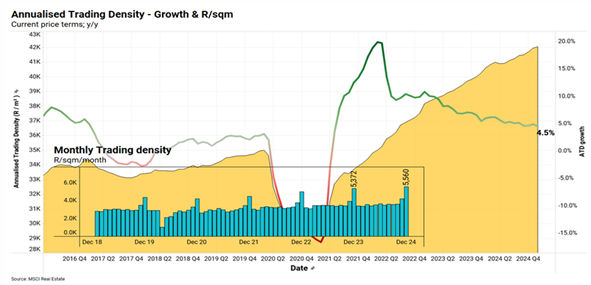

In the retail sector, the benchmark is to measure how much total revenue a tenant can make per square metre that they occupy. The higher the revenue per square metre, the better will be the trading density, and the more profitable the tenant is likely to be. This also measures how each tenant is doing in different geographies around the country. The following graph reflects the annualised trading density – from 2018 to the end of 2024. As one can see there was a blip in 2020 due to the limited trading activity brought on by Covid-19, during the lock down. The annual trading density growth is around 4,5% driven by inflation and volume growth.

OFFICE SECTOR: STILL SOME WAY TO GO TO FULL RECOVERY

Office rentals have been declining while other sectors delivered real growth – what has been highlighted by the results to 31 December 2024, is that office rentals are still under pressure and that the recovery is in specific areas. Rental growth is exceeding inflation in all sectors except offices, while vacancies remain flat throughout. The office sector continues to be a laggard, but there are some areas of recovery. SA’s office vacancy rate recorded 13.7% during Q4 2024, up 10 basis points from Q3 2024 according to SAPOA’s Office Vacancy Survey – the first increase since Q2 2022 when vacancies peaked at 16.7% followed by an improvement for nine consecutive quarters. Despite the marginal deterioration in vacancies, growth in asking rentals accelerated to 2.2% year-over-year and while this is well below inflation, it may signal that overall supply and demand is edging closer to equilibrium.

The graph below highlights a consolidated sector index, by taking all the properties in a sector and applying the rental growth.

INDUSTRIAL SECTOR: DEMAND FOR LOGISTICS PROPERTIES REMAINS ROBUST

The industrial and logistics property market continues to grow – a growth derived from the continued rise of e-commerce and shifts in global supply chains. All industrial hubs, including notable sites like Waterfall’s distribution hub, Longmeadow, and Durban’s Cornubia and Umgeni Business Park, are performing very well, with low vacancies and strong rental growth.

This targeted investment approach signals rising optimism in the logistics property sector. The market’s vitality is highlighted by strong occupancy rates and ongoing rental growth, as more businesses prioritize the expansion of their warehousing and distribution networks.

OUTLOOK AND STRATEGIC IMPLICATIONS FOR THE LISTED PROPERTY SECTOR

South Africa’s listed property sector is in a good position to benefit from positive local and global trends in the second quarter. The South African Reserve Bank’s carefully considered approach to easing interest rates, along with a stronger rand, supports continued investor interest in property assets. The significant reduction in loadshedding and improving vacancies across the board is expected to bear positive effects on listed property stocks.

Stable inflation could drive more demand for income-generating assets like property stocks and bonds. Although these developments are encouraging, the property sector continues to contend with challenges such as infrastructure constraints, elevated unemployment, and increasing energy expenses.

In short, the first quarter and rest of 2025 has reflected both challenges and even better opportunities. Going forward, staying adaptable and focusing on growth areas will be the key to maintaining this positive trend and delivering value for investors, backed by strong investor support and an improving economic environment. Listed property is still trading at substantial discounts to Net Asset Value (NAV), and over time, prices should catch up to the true intrinsic value of the underlying properties.

We ask you to be safe, and feel free to contact us with any questions. We appreciate your support and confidence in us, in being able to manage and grow your wealth.

This targeted investment approach signals rising optimism in the logistics property sector. The market’s vitality is highlighted by strong occupancy rates and ongoing rental growth, as more businesses prioritize the expansion of their warehousing and distribution networks.

Vuyani Bekwa – Principal: Private Equity

Vuyani is an experienced real estate and investment professional, recognized for his strategic leadership in fund and asset management, private equity, property, and renewable energy. He is an ex-Portfolio Manager at Investec Asset Management (now Ninety One), where he managed the award-winning Investec Property Equity Fund and institutional mandates, ex-Fund Manager for Liberty’s Property Portfolio (R30bn), and oversaw three private equity funds at Eris Property Group (R8bn). Vuyani holds a Bachelor’s degree in Public Administration (Economics) from the University of the Western Cape, a Post-Graduate Diploma in Business Management, and an MBA in Strategic Financial Management, both from UKZN. He also holds FAIS-recognized RE 5 certification.