Before all else, a note from our Founder & CEO

As global economic uncertainty intensifies, our fourth quarterly update explores how South Africa-focused listed property could see a reassessment in investor sentiment. In times like these, locally grounded assets may start to look more attractive. Vuyani Bekwa, Principal – Private Equity, weighs in on the resilience of the domestic property market. He highlights several key tailwinds contributing to its continuing delivery.

THE SOUTH AFRICAN LISTED PROPERTY SECTOR IN Q4 2025:

The performance of the South African listed property in Q4 2025 was marked by a strong return of 16.7% pushing the total returns to 30.6% for the calendar year. This performance was driven by a sharp rally in South African government bonds, which significantly re-rated. The benchmark 10-year bond yield declined from 10,28% to 8,32% over the quarter, supported by several structural and cyclical tailwinds. The SA Reserve Bank adopted an inflation target of 3%, which strengthened their credibility in the market, anchoring inflation expectations and reducing the country’s risk premium. Higher commodity prices, such as gold, improved the fiscal outlook via stronger tax receipts, and the removal of the country from the Financial Action Task Force ‘grey list’ reduced systematic risk. Standard & Poors, the global ratings agency, upgraded the sovereign currency rating to BB, leading to an increase in the JP Morgan Emerging Market Bond index. This drove global inflows into SA bonds and lifted all other asset classes.

The performance of the listed property was also influenced by the broader market trends, with equities (FTSE/JSE All Share Index) outperforming property, returning 42.4%. Equities were driven by the resources sector (FTSE/JSE Resources 10 index, which delivered, +144%) as commodity prices surged.

The investment environment continues to improve, and the table below is a sample of some of the REIT stocks where we have exposure. These returns exclude distributions paid over the past 12 months:

Property delivered a solid 30.60% return for investors for the calendar year 2025 but was weaker than equity stocks (up 42.40%), but higher than bonds (up 24.20%). That strong showing came from a mix of rising property values, steady rental income and a re-rating of SA government bonds. It is a sign that South African property is recovering and looking attractive again, especially with interest rates easing and economic growth picking up, even if slightly.

Below we provide a concise overview of developments in the fourth quarter of 2025, focusing on key economic trends, sectoral performance, and the outlook for the period ahead.

GLOBAL MACRO CONTEXT AND MARKET TRENDS

Equities

U.S. stocks posted solid gains in Q4, with indexes like the S&P 500 advancing modestly and finishing the year with robust overall returns. The S&P 500 was up for the quarter and ended 2025 on strong footing following positive earnings and resilient consumer demand. Broader U.S. gains were helped by resilient corporate earnings, especially from large-cap growth and tech stocks, though volatility remained elevated at times. Concerns over stretched valuations — especially in mega-cap tech — were a recurring theme, resulting in some profit-taking and heightened sector rotation.

Global Equities

International markets outpaced U.S. equities in the quarter and year overall, driven by strong gains in Europe, Asia, and emerging markets. Global equity benchmarks such as the MSCI ACWI ex-USA delivered notable gains and were a highlight for diversified investors in 2025.

Emerging markets, particularly in Asia, exhibited impressive returns, supported by robust growth expectations and relative valuation appeal versus developed markets.

Commodities

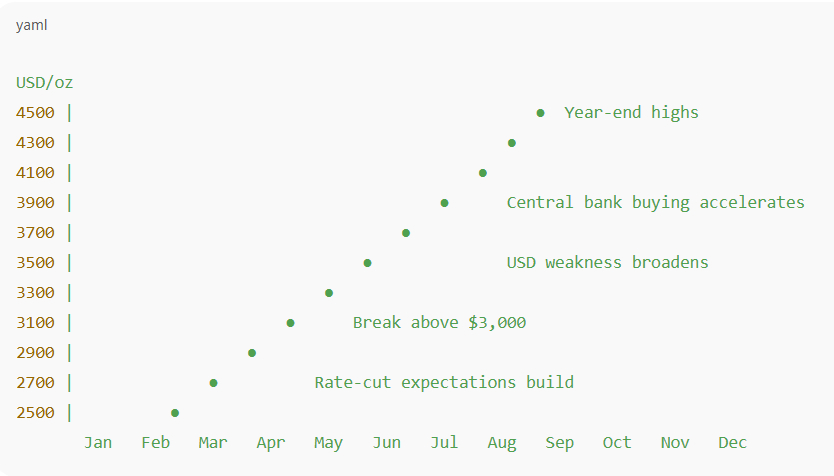

Precious metals surged, with gold and silver posting significant gains, reflecting their safe-haven appeal. This is reflected in the continuing increase in the gold price as can be seen from the chart below (with notations):

Price Highlights

• Start of Year: Gold began 2025 near $2,620–2,650/oz on 1 January.

• Mid-Year Rally: Prices climbed past $3,000/oz by mid-March and continued higher through spring and summer, breaking numerous historical thresholds in succession — including $3,100, $3,200, $3,300 and eventually above $3,800 by late September.

• Year-End Levels: Strong momentum carried gold toward the end of December, with closing prices around ~$4,300+ per ounce on 31 December 2025, reflecting a ~64%+ annual increase.

• Annual Return: According to the World Gold Council Gold Market Commentary, gold delivered exceptionally strong year-to-date returns in 2025 (over 60% in USD), with record prices reached across many currencies by year-end.

This performance represented one of the strongest yearly rallies in decades as investors progressively shifted to precious metals amid macroeconomic and geopolitical concerns.

Monetary Policy & Interest Rates

Major central banks, including the Federal Reserve, shifted toward more accommodative stances late in 2025 as economic growth showed signs of moderation. Rate cuts were either delivered or priced into markets, helping support risk assets. The U.S. labour market showed signs of softening, reducing inflationary pressures and bolstering expectations for lower rates, though the services sector remained resilient.

Inflation & Economic Growth

Inflation continued to ease in key regions, while consumer spending remained a key driver of economic resilience in the U.S. Global growth prospects were bolstered by supportive fiscal policies in Europe and stimulus efforts in Japan, even as geopolitical risks and trade uncertainty persisted.

Currency & Commodities

The U.S. dollar weakened against major currencies during the quarter and into early 2026 — an important theme for global markets, boosting foreign earnings for U.S. multinationals and supporting non-U.S. equity performance. Oil prices were pressured by higher inventories and softening demand signals, while gold reached multi-year highs as investors sought shelter from policy uncertainty and currency declines.

Sector & Regional Highlights

Technology & AI

Technology and AI-related stocks continued as dominant market drivers, with strong earnings results from major players and continued investment in generative AI and data centre capacity. However, tech valuations triggered debate about sustainability and rotation into value and cyclical sectors.

International Markets

European and emerging market equities delivered robust returns, assisted by easing inflation, fiscal stimulus in key economies, and attractive valuations. China’s market underperformance moderated global EM returns, though broader Asian markets remained strong.

Sector Rotation & Commodities

Precious metals outperformed many asset classes, driven by safe-haven demand and currency trends. Energy markets faced pressure from oversupply concerns, while commodities overall showed mixed performance.

Market Sentiment & Risks

Earnings Strength vs. Policy Uncertainty

Corporate earnings generally exceeded expectations, providing fundamental support for equities even amid macro scepticism. Nonetheless, ongoing trade policy uncertainty, geopolitical tensions, and questions about the durability of the growth cycle contributed to periodic volatility and investor “wall of worry” dynamics.

Summary

Q4 2025 was characterized by:

• Resilient equity gains in both U.S. and global markets despite macro uncertainties.

• Monetary easing expectations supporting risk assets and fixed income.

• Global diversification benefits, with international and emerging markets notably outperforming.

• Tech/AI leadership, valuations debates, and safe-haven flows into metals and quality assets.

THE DIRECT PROPERTY SECTOR: HOW HAS IT FARED – PERFORMANCE AND INSIGHTS

RETAIL SECTOR: MERGERS AND ACQUISITIONS – A CASE STUDY

Hyprop’s planned sale of 50% of Hyde Park Corner for R805 million in July 2025 to Millennium Equity Partners has ultimately collapsed, with the deal officially terminated in January 2026 after the buyer failed to meet transaction conditions. This leaves Hyprop still owning the entire Hyde

Park Corner asset, despite its strategic intent to recycle capital into the Western Cape and Eastern Europe.

Key Details of the Transaction

Asset: Hyde Park Corner, a 38,257 m² shopping centre in Johannesburg, one of Hyprop’s oldest and most prestigious properties.

Initial Plan (July 2025): Hyprop announced the sale of a 50% undivided share plus rental enterprise for R805 million.

Buyer: Millennium Equity Partners (MEP), a relatively small private property company with limited retail holdings.

Strategic Rationale: Hyprop aimed to free up capital to focus on Western Cape retail hubs (like Canal Walk and Somerset Mall) and expand further into Eastern Europe, where it already owns assets.

Future Plan: Hyprop had indicated it might sell the remaining 50% within two years, effectively exiting Hyde Park Corner.

Outcome (Jan 2026): The deal was terminated as Millennium Equity Partners could not fulfil transaction conditions.

Strategic Implications

Capital Recycling Blocked: Hyprop’s strategy to redeploy funds into higher-growth regions is delayed. This could slow its portfolio rebalancing away from Gauteng.

Market Confidence: The collapse highlights risk of partnering with smaller, less capitalized buyers in large-scale property transactions.

Asset Retention: Hyde Park Corner remains a prime Sandton retail destination, meaning Hyprop still benefits from its rental income and prestige, but also remains exposed to Gauteng’s slower retail growth compared to Cape Town and Eastern Europe.

The attempted sale of Hyde Park Corner illustrates both the ambition and challenges of South African REITs in repositioning their portfolios. While Hyprop’s intent to shift capital into higher-growth regions is sound, execution risk remains high when counterparties lack financial depth. For investors, the failure underscores the importance of transaction certainty in property deals. For Hyprop, retaining Hyde Park Corner may not be disastrous – it remains a blue-chip retail asset – but it does slow the company’s strategic pivot.

When looking at our exposure to Hyprop, because of our fundamental call on retail, we have it and are overweight when compared to the benchmark, sitting at 7% of the portfolio. Management have moved

in the right direction and understand the portfolio well and continue to derive good earnings growth going forward.

INDUSTRIAL SECTOR: DRIVEN BY MANUFACTURING GAINS DESPITE INFRASTRUCTURE CHALLENGES

Mixed Performance: Production vs Confidence

• Manufacturing output remained weak at the end of 2025. Official data show overall industrial production and manufacturing output declining about 1 % in November 2025 compared to the prior year, with some sub-sectors like wood products, metals and machinery, and motor vehicles particularly soft. However, there was some sequential quarterly increase in output in the three months to November 2025 versus the prior quarter.

• Business confidence improved materially in Q4, with the RMB/BER confidence index rising to 44 points, up from a one-year low of 39 in Q3. This was the first rebound after two consecutive declines and suggests sentiment is stabilising in the broader business environment.

Although production remains subdued and at times contractionary, firms are somewhat more optimistic about future activity — a necessary condition for investment decisions.

Macro-economic context

• South Africa’s GDP grew about 1.8 % in Q4 2025, reflecting resilience overall but highlighting that industrial sectors were not the main growth drivers — services and mining made stronger contributions.

• Business sentiment gains are positive, but cautious: a confidence index below 50 still implies that many firms see conditions as challenging relative to long-term benchmarks.

Outlook Implications

Short term:

The industrial sector is likely to remain uneven in early 2026, with output subdued and selective improvements in sectors tied to external demand (mining, some metals). A rebound in business confidence is a necessary but not sufficient condition for strong industrial recovery.

Medium term:

Policy interventions (e.g., automotive production support) and improvements in energy supply could help stabilise industrial activity. Structural reforms addressing logistics, investment incentives, and production competitiveness will be key to a sustainable rebound.

OFFICE SECTOR: SLOW RECOVERY AMID SHIFTING WORK PATTERNS

Office Picture

South Africa’s office vacancy rate declined to 12.8% in Q4 2025, the lowest since late 2020 according to SAPOA’s Office Vacancy Survey Report for Q4 2025 – and reflecting steady gains across several major nodes despite structural pressure in weaker markets. The peak overall vacancy was in June 2022 at 16.8%.

There is divergent performance by grade, with demand remaining strongest in Prime and A-grade offices, where vacancies fell to 5.8% and 10.8% respectively, reflecting ongoing occupier preference for modern, flexible, hybrid-ready space. In contrast, C-grade stock weakened to 16.5%, and large portions of B-grade offices remain under severe pressure.

Regional disparities of course persist, with Cape Town Metro sustaining its position as the best-performing market with a 6.3% vacancy rate, well below pre-pandemic levels. Notably, all of Cape Town’s office nodes now have vacancy levels below where they were when the national office vacancy rate peaked in Q2 2022, signalling consistent demand and effective stock absorption in the region. Johannesburg Metro, despite improvement, remains the city with the highest overall office vacancy rate at 16.5%, though much improved since its peak of 19.5% recorded in mid-2022. Despite the recent improvement, the city’s office vacancy rate remained well above its pre-pandemic level of 12.5%, reflecting continued challenges in absorbing excess stock across various nodes as many occupiers’ space requirements has changed.

Durban Metro’s vacancy rate improved to 12.4%, below its 2019 level. Much of this recovery has been driven by better-quality decentralised stock, particularly in the prime segment, which has returned to levels last seen in 2018.

Office development activity remains limited due and most new office projects remain tenant driven with very limited speculative development. Projects are largely tenant-driven with limited speculative activity, and the pre-let rate has eased to 55.6% from 71.4%. Troubled assets continue to weigh on recovery, with over half of all vacant office space concentrated in buildings that are at least 50% empty, particularly in the B-grade segment. These assets face structural and financial hurdles, pressuring rentals in weaker nodes.

While the vacancy rate has improved, the absolute level of vacant space exceeds 2.4 million sqm—significantly higher than in past cycles – indicating that oversupply continues to cap rental growth and valuations.

We ask you to be safe, and feel free to contact us with any questions. We appreciate your support and confidence in us, in being able to manage and grow your wealth.

Vuyani Bekwa: Principal – Private Equity

Vuyani is the Principal – Private Equity with strong expertise in listed property, asset management, fund management and private equity. He holds a B Admin (Economics), University of Western Cape, a Post-Grad Diploma in Business Management and a Master-in-Business Administration (MBA) Strategic Financial Management, both from University of KwaZulu-Natal. He also has a FSCA accreditation with the RE5 certification.

He began his career as an economic researcher for South Africa’s first socially responsible unit trust in 1995. He then moved into listed property and equity investment analysis when he moved to Marriott Asset Management (now part of Old Mutual Investment Group) in 1997. He then spent 6 years managing listed property portfolios and being the portfolio manager for the Investec Property Equity Fund (now part of Ninety-One). He has spent the last twelve years focusing on private equity structures, either setting up or managing capital into funds, some with an impact focus. He is currently busy focusing on the MSM Infrastructure Impact Fund, which is looking for exposure into Industrial and infrastructure assets.