A note from our Founder & CEO

“As global economic uncertainties intensify, our first quarterly update for 2026 explores how South Africa-focused listed property could see a reassessment in investor sentiment. In times like these, locally grounded assets may start to look more attractive.”

Vuyani Bekwa, Principal – Private Equity, weighs in on the resilience of the domestic property market. He highlights several key tailwinds contributing to its continuing delivery.

THE SOUTH AFRICAN LISTED PROPERTY SECTOR IN Q1 2026:

The South African listed property sector delivered mixed returns during the quarter, with a sharp pullback in March offsetting gains made earlier in the year. Listed property markets were volatile during March 2026 due to global risk aversion amid geopolitical uncertainties. Despite share price volatility, underlying portfolio fundamentals improved during the quarter, including declining vacancies, stable tenant collections and improved balance sheets. Industrial‑focused REITs and domestically oriented portfolios continued to outperform office‑heavy counters.

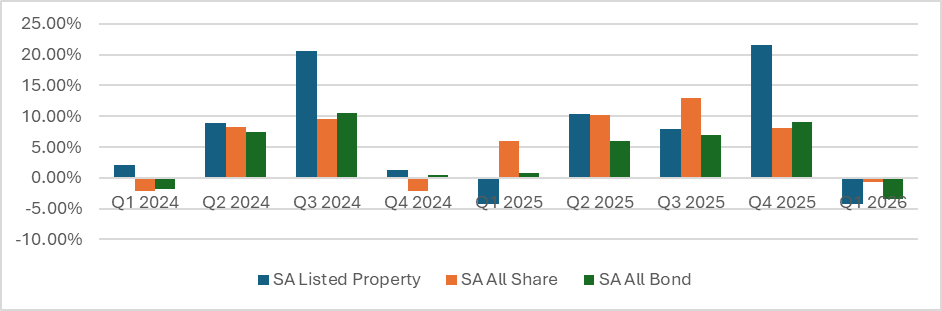

SA Asset Class Performance to 31 March 2026

SA Listed Property delivered a weaker quarter (weak, but positive January (0.9%), even stronger February (8.1%), but March wiped out those returns, (-12.3%), resulting in a negative 4.34%. This was in line with bonds (-3.41%) and equities (-0.69%), as both also delivered negative returns for the quarter. Here is a performance graph of all the individual stocks in the SA Listed Property index.

The SA Reserve Bank (SARB) held the repo rate steady at 6.75% on 29th January 2026, noting CPI slowed to 3.2% y/y in December – near the upper target band of 3% – helping funding visibility, sector sentiment and setting the scene for the strong returns for February. This also implied that, ceteris paribus, that interest rates would decline at the next SARB MPC meeting on 26th March 2026. However, the SARB never dropped interest rates due to the war in Iran.

GLOBAL MACRO CONTEXT AND MARKET TRENDS

The global macro context and market trends for Q1 2026 were characterized by a mix of optimism and caution. Markets shifted notably in Q1 2026 as investors grappled with rising energy prices, sector rotation, and growing uncertainty around the pace of global monetary easing. The optimism that characterised the final months of 2025 began to fade as commodity markets surged and equity leadership rotated. Energy stocks emerged as the clear outperformer across global markets, while technology and consumer sectors lost momentum. At the same time, bond markets experienced renewed volatility as investors reassessed inflation risks and the timing of interest rate cuts.

MACROECONOMIC LANDSCAPE

United States

The US economy entered 2026 with moderate momentum, but increasing uncertainty around the path of monetary policy. Consumer spending and a resilient labour market continued to support activity, although higher borrowing costs weighed on housing and corporate investment. Inflation pressures persisted into Q1, particularly as energy prices rose sharply, complicating the Federal Reserve’s policy outlook. Policymakers maintained a cautious tone, emphasising a data-dependent approach as they balanced the risks of easing too early against slowing growth.

Europe

Economic conditions across the euro area remained subdued. Industrial production continued to face pressure from weak external demand and elevated energy costs, while services activity provided only limited support.

The European Central Bank maintained a cautious stance, balancing slower growth with inflation that remained above target in several economies. Fiscal consolidation across parts of the region further contributed to a restrained economic backdrop.

Asia & Emerging Markets

Across Asia and emerging markets, performance remained uneven. Japan benefited from stable domestic demand and continued corporate reform momentum, supporting moderate growth.

In contrast, China’s recovery remained fragile, with structural challenges in the property sector and cautious consumer sentiment weighing on activity. More broadly, emerging markets remained sensitive to global capital flows and commodity price movements.

Overall, the macro backdrop in Q1 reflected a global economy that remained positive but fragile, leaving markets increasingly sensitive to commodity shocks, policy signals, and inflation developments.

THE WIDER ECONOMY – PERFORMANCE AND INSIGHTS

South Africa’s Gross Domestic Product (GDP) for Q4 2025 revealed a year-on-year growth rate of 0.9%, in line with expectations but still weaker in the broader economic context. While a technical recession was avoided, economic growth continues to lag population expansion, keeping the country in a per capita recession.

Sector Performance and Key Drivers

Agriculture rebounded significantly in Q4, growing by 17% due to a base effect after a sharp contraction in Q3 of 2024. However, agriculture remains a highly volatile sector, and while its strong performance in Q4 contributed nearly 50% of the quarter’s overall growth, it does not reflect a sustainable driver of economic expansion. Other contributors to economic activity included trade, catering, and accommodation, which benefited from a recovery in tourism, along with finance and real estate. However, key productive sectors such as mining and manufacturing continued to decline, highlighting the uneven nature of growth in the economy.

Consumer Spending and Investment Trends

Despite high unemployment rates, inflationary pressures, and interest rates remaining elevated, consumer spending increased for the third consecutive quarter. Consumers showed some resilience despite economic headwinds, with clothing and footwear seeing a notable 4.4% increase in spending. The two-pot pension withdrawal system also provided a short-term boost to household consumption, but it is not a sustainable source of long-term growth.

Investment concerns remain high as gross fixed capital formation, an essential indicator of economic reinvestment recorded another negative quarter. The continued decline in investment, particularly in residential construction, reflects weakened business confidence and limited long-term growth prospects.

Infrastructure and Global Trade Dynamics

Loadshedding relief provided a small boost to economic activity in Q4, as power disruptions were significantly lower than in previous quarters. However, infrastructure constraints, particularly at ports and railways, continue to hinder economic momentum. The easing of loadshedding was a welcomed development, but broader infrastructure challenges remain a significant drag on growth. While global trade dynamics had minimal impact in Q4, rising geopolitical tensions, especially in relation to the United States (US), pose risks for SA’s trade relationships in 2025.

In the medium-term budget statement, National Treasury supported the SA Reserve Bank’s lowering of the inflation target to 3%. The intention is to ensure a tighter range which will give more certainty on inflation. For February, inflation dropped to 3%, indicating that the SA Reserve Bank should have dropped interest rates, but geopolitical risks had risen so much that it held back to understand the impact of higher oil prices on local inflation.

THE DIRECT PROPERTY SECTOR: HOW HAS IT FARED – PERFORMANCE AND INSIGHTS

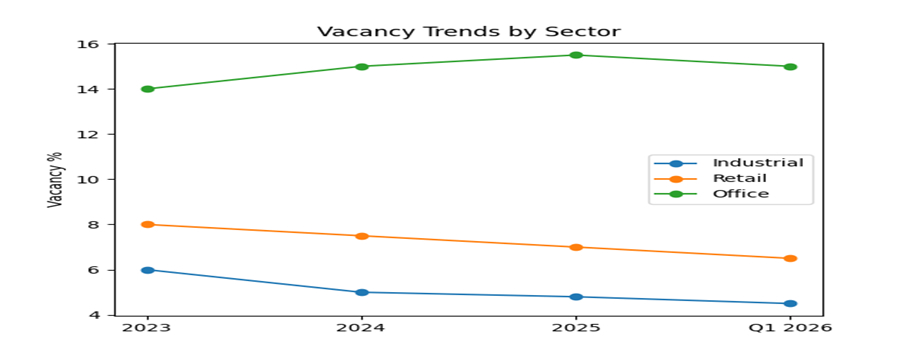

Direct property markets continued to stabilise across all major sectors. Vacancies trended lower nationally (as per graph below), supported by improved tenant demand and disciplined new supply. Performance remained node‑specific, with well‑located and higher‑quality assets outperforming.

RETAIL SECTOR:

- Retail property fundamentals continued to improve in Q1 2026, supported by resilient consumer spending and improved footfall.

- Vacancies have declined to approximately 6–7%, with stronger performance in convenience and township retail formats.

- Super-regional malls continue to recover, although rental growth remains modest.

INDUSTRIAL SECTOR: CONTINUES TO DELIVER

- The industrial sector remains the strongest-performing segment of the market, supported by logistics demand, e-commerce growth, and supply chain optimisation.

- Vacancy rates remain low (circa 4–5%), with positive rental growth observed across major nodes.

- Development activity is increasing, particularly in logistics parks and last-mile distribution facilities.

OFFICE SECTOR: VACANCY IMPROVING IN LEAPS AND BOUNDS

- The office sector remains under pressure, with elevated vacancies (circa 14–16%) and limited rental growth.

- Decentralisation trends and hybrid working models continue to impact demand.

- Adaptive reuse and conversions to residential remain key themes. This is taking place around the country where there is residential demand.

OUTLOOK AND STRATEGIC IMPLICATIONS FOR THE LISTED PROPERTY SECTOR

South Africa’s listed property market continues to show improving dynamics, with retail and industrial properties performing strongly, which has helped boost confidence across the sector. While offices are gaining traction, they are still lagging.

We ask you to be safe and feel free to contact us with any questions. We appreciate your support and confidence in us being able to manage and grow your wealth.

Vuyani Bekwa: Principal – Private Equity

Vuyani is the Principal – Private Equity with strong expertise in Listed Property, Asset Management, Fund Management and Private Equity. He holds a B Admin (Economics), University of Western Cape, a Post-Grad Diploma in Business Management and a Master-in-Business Administration (MBA), both from University of KwaZulu-Natal. He also has a FSCA accreditation with the RE5 and RE3 certification.

He began his career as an Economic Researcher for South Africa’s first socially responsible unit trust in 1995. He then moved into Listed Property and Equity Investment Analysis when he moved to Marriott Asset Management (now part of Old Mutual Investment Group) in 1997.

He spent 6 years managing listed property portfolios and being the portfolio manager for the Investec Property Equity Fund (now part of Ninety-One). He has spent the last ten years focusing on private equity structures; setting up or managing capital into funds and some with an impact focus. He is currently focusing on the MSM Infrastructure Impact Fund, which is looking for exposure into Industrial and Social Infrastructure Assets.